Revealing that which is concealed. Learning about anything that resembles real freedom. A journey of self-discovery shared with the world.

Have no fellowship with the unfruitful works of darkness, but rather reprove them - Ephesians 5-11

Join me and let's follow that high road...

Monday, February 24, 2020

Chinese Business Conditions Crash Most On Record

For the past two weeks, even as the market took delight in China's

doctored and fabricated numbers showing the coronavirus spread was

"slowing", we warned again and again that not only was this not the case

(which was confirmed by the latest data out of South Korea, Japan and

now Italy), but that for all its assertions to the contrary, China's

workers simply refused to go back to work (even with FoxConn offering its workers extra bonuses just to return to the factory) and as a result the domestic economy had ground to a halt, something we described previously in:

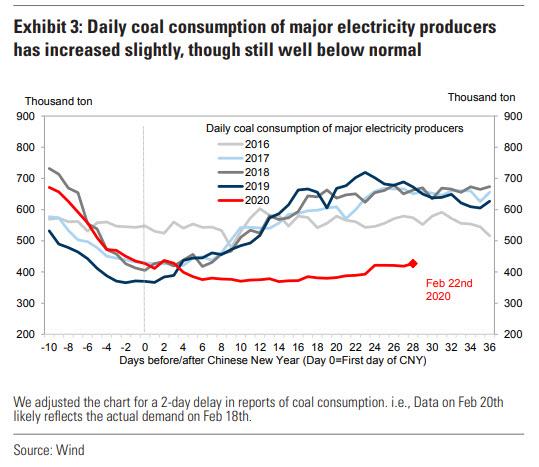

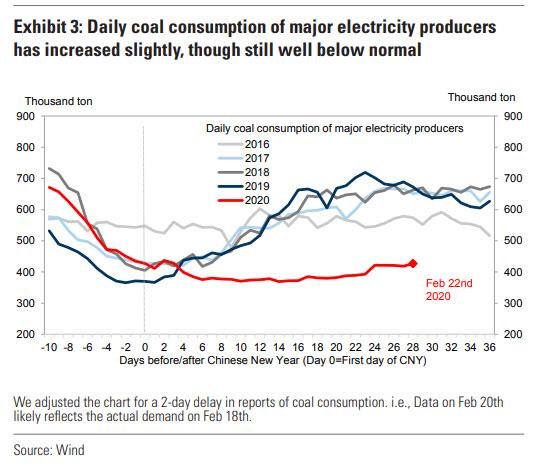

Unfortunately, one month after the start of the Lunar New Year it's not getting any better, as the latest high frequency updates out of China, courtesy of Goldman Sachs, demonstrate. First, here is China's daily coal consumption which have barely

pushed off the lows, and are roughly 50% where they were a year ago this

time.

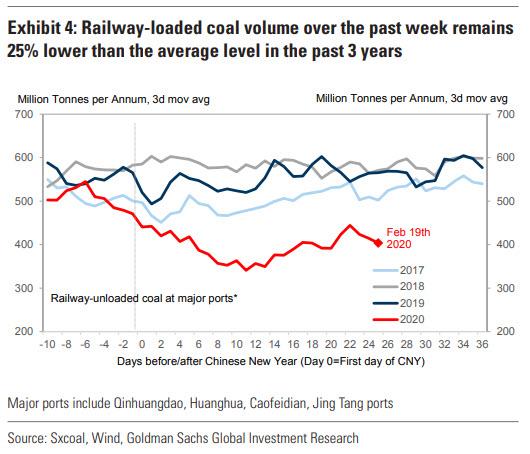

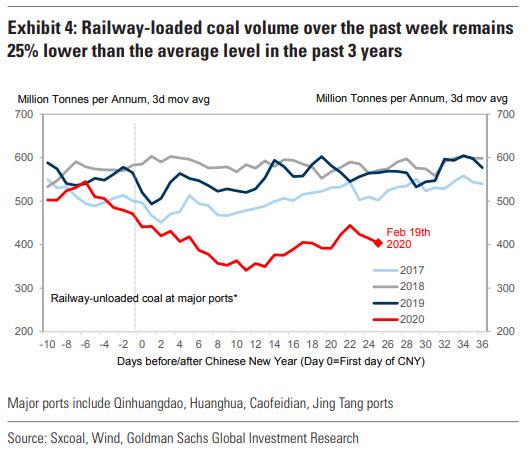

With coal demand in the doldrums, it is also to be expected that coal

supply is depressed as well, and indeed coal volumes over the past week

remain 25% lower than the past 3 years' average, and roughly 33% below

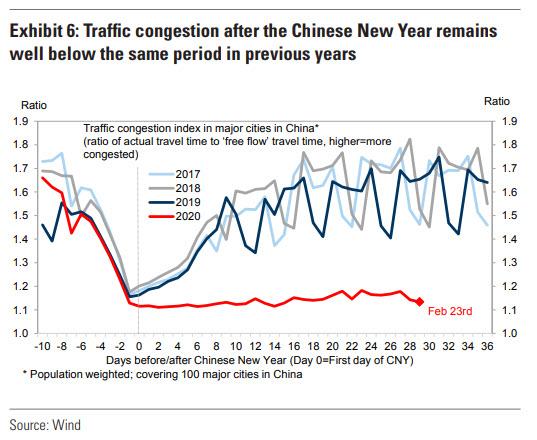

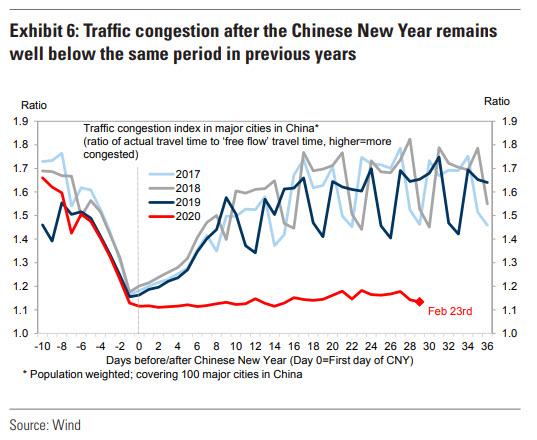

the 2019 level. One of the better indicators of real-time commerce, traffic

congestion, remains virtually unchanged, and substantially below where

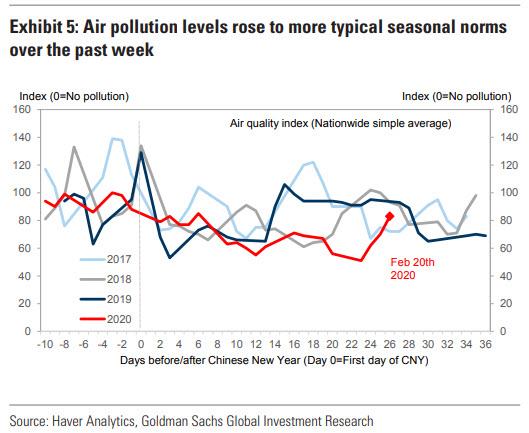

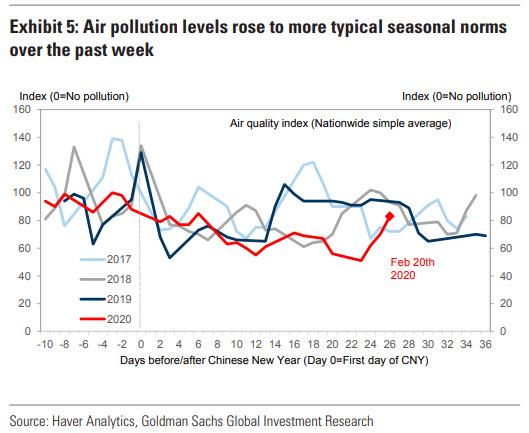

it was in previous years. Yet, hilariously, this being China even with no transport, no

commerce, and virtually no power plant use, pollution is finally

starting to ramp up. One wonders what is causing this if it's not coal

demand, or transportation: maybe all those crematoriums working

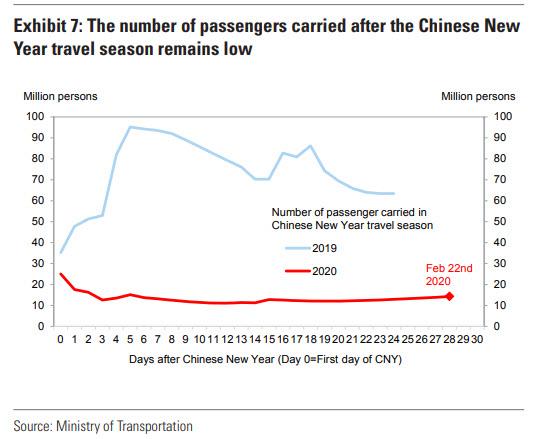

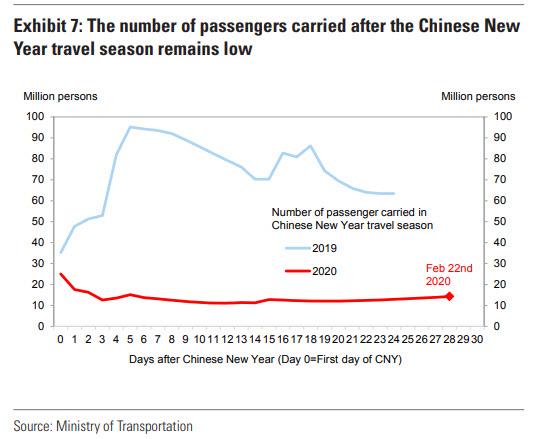

overtime? And speaking of not transport, the number of passengers carried after

the New Year is barely above 10 million, almost 50 million below last

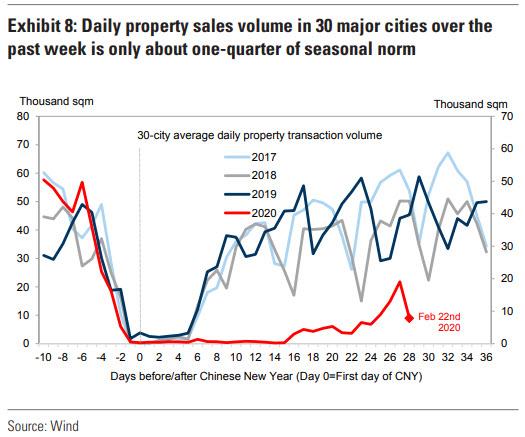

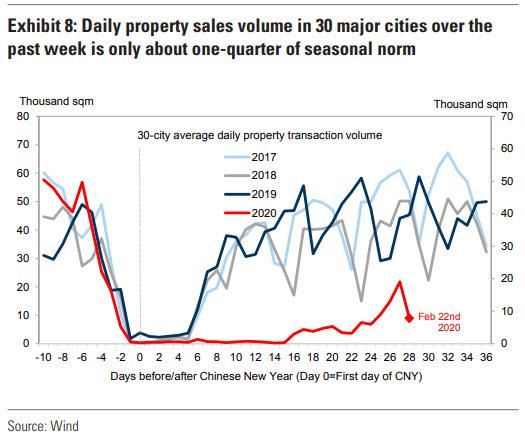

year's levels. Meanwhile, a brief silver lining in the economy was promptly snuffed

out last week, when the property sales volume in 30 major cities crashed

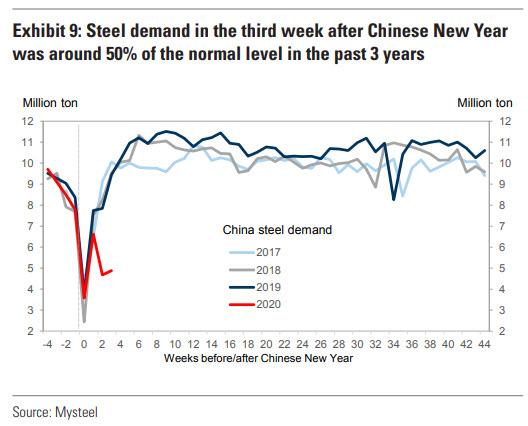

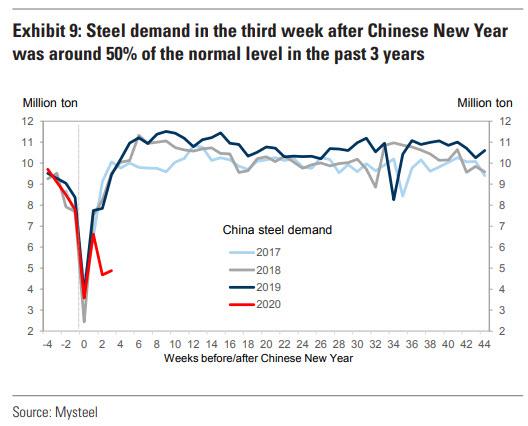

back to earth and remains well below 25% of the seasonal norm. And with no end market demand, it is hardly a surprise that steel

demand has continued to crater, and was below half the normal level from

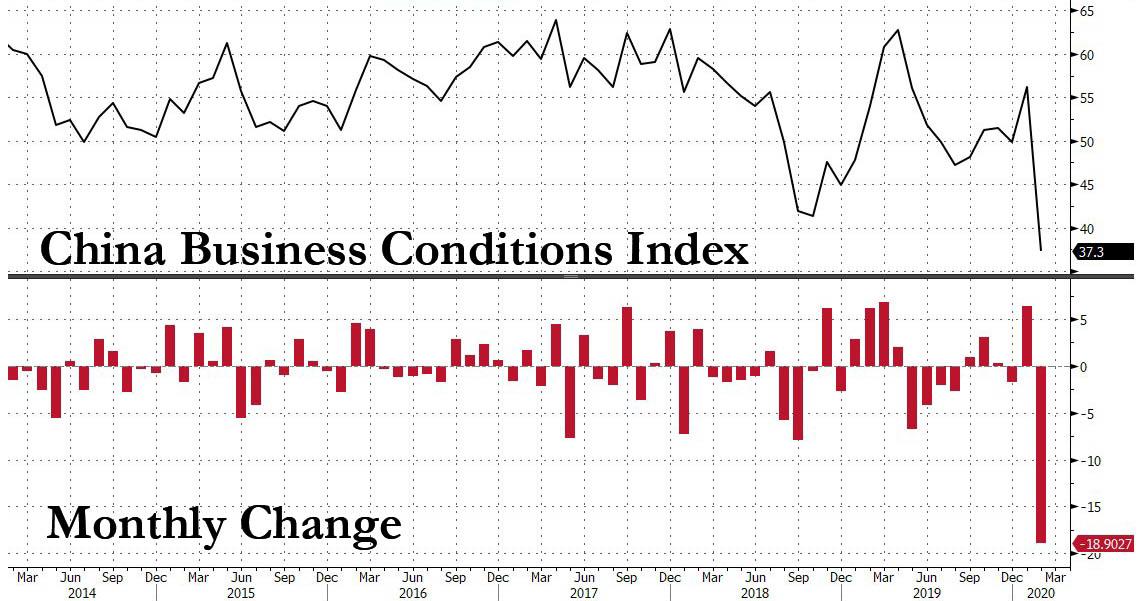

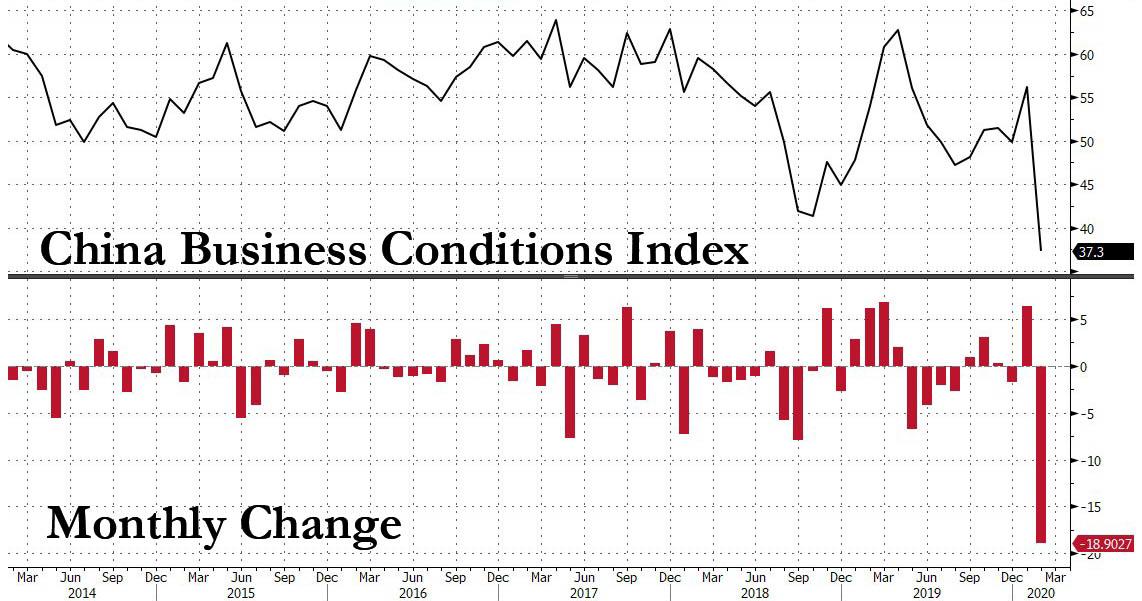

the past 3 years. Last but not least, and perhaps most ominous of all, the earlier

semi-official data print in the form of the February survey on business

conditions showed a depression level plunge, with the index crashing

more than 18 points, the most on record, to 37.3, which confirms Nomura's expectation of a manufacturing PMI print later this week which may have a 30-handle.